本文在上一篇文章(vectorbt学习_17DMA之三滑窗网格参数优选)面临问题

时间切分后,根据切分后的行情数据,重新计算技术指标,会存在一部分行情作为技术指标的预热时间被消耗掉。

比如:训练集,验证集时间(80,40), slow_windows=30,慢均线需要30天才有有效值。

则意味着训练集需要只有50(80-30)天,预测集10(40-30)天,技术指标slow_ma有有效取值。实际训练,验证集为(50,10),与本意偏差较大。

勘误:此篇文章部分截图可能有误,此文章的后继文章“DMA之六滑窗网格参数优选”修复此问题。请查阅后文。

01,基础配置信息

1 | #conda envs:vectorbt_env |

02,行情获取和可视化

a,时间交易参数配置

1 | # Enter your parameters here |

b,获取行情和行情mask

1 | # Download data with time buffer |

origin ohlcv_wbuf size: (978, 5)

Index(['Open', 'High', 'Low', 'Close', 'Volume'], dtype='object')

wobuf_mask ohlcv size: (728, 5)

20,网格参数-指标计算和可视化

仅可视化第一列

1 | price=ohlcv_wbuf['Close'] |

(978, 780)

(978, 780)

(728, 780)

(728, 780)

21,网格参数-信号计算和可视化

仅可视化第一列

dmac_size.shape: (728, 780)

dmac_size.iloc[:3,:3]:

fast_window 10

slow_window 11 12 13

date

2020-01-02 00:00:00+00:00 True True True

2020-01-03 00:00:00+00:00 True True True

2020-01-06 00:00:00+00:00 True True True

Start 2020-01-02 00:00:00+00:00

End 2022-12-30 00:00:00+00:00

Period 728

Total 423.078205

Rate [%] 58.115138

First Index 2020-01-02 02:00:00+00:00

Last Index 2022-12-27 06:59:04.615384576+00:00

Norm Avg Index [-1, 1] -0.179136

Distance: Min 1.0

Distance: Max 75.946154

Distance: Mean 1.720602

Distance: Std 5.889353

Total Partitions 14.607692

Partition Rate [%] 3.501842

Partition Length: Min 3.239744

Partition Length: Max 85.138462

Partition Length: Mean 36.392118

Partition Length: Std 27.476308

Partition Distance: Min 4.425641

Partition Distance: Max 75.946154

Partition Distance: Mean 29.174564

Partition Distance: Std 26.152924

Name: agg_func_mean, dtype: object

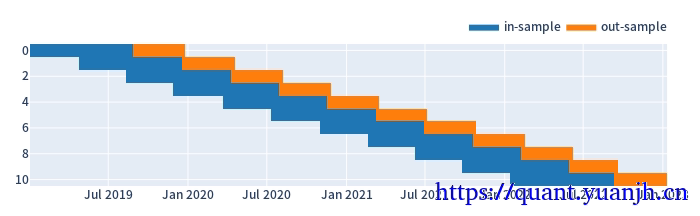

22,行情,信号的滑窗处理

注意点:

01,训练集和验证集比例3:1,或者2:1,对应:window_len和set_lens为4:1(或3:1),过大了历史包袱沉重,无法及时响应最新行情,过小了则容易参数跳变,形成类似过拟合效果

a,参数设置和效果预览

代码中

1 | # todo这里是自然日计算的,但后面训练,验证集个数计算都完全正确,哪里应该和预想的不一致 |

1 | # 滚动周期参数设置和大致效果可视化 |

split_kwargs: {'n': 11, 'window_len': 240, 'set_lens': (80,), 'left_to_right': False}

in_price.shape: (160, 11)

out_price.shape: (80, 11)

in_price.index: RangeIndex(start=0, stop=160, step=1)

in_price.columns: Int64Index([0, 1, 2, 3, 4, 5, 6, 7, 8, 9, 10], dtype='int64', name='split_idx')

in_price[0:3]: split_idx 0 1 2 3 4 5 6 7 8 9 10

0 49.17 58.15 51.20 43.39 48.15 97.90 167.98 239.52 202.00 251.77 253.14

1 48.06 56.16 49.50 43.15 49.73 96.55 164.08 225.00 214.11 252.50 266.49

2 50.65 55.36 50.29 43.79 52.25 94.50 168.03 208.99 227.02 246.86 266.08

in_indexes[:5]: [DatetimeIndex(['2019-01-02 00:00:00+00:00', '2019-01-03 00:00:00+00:00', '2019-01-04 00:00:00+00:00', '2019-01-07 00:00:00+00:00', '2019-01-08 00:00:00+00:00', '2019-01-09 00:00:00+00:00', '2019-01-10 00:00:00+00:00', '2019-01-11 00:00:00+00:00', '2019-01-14 00:00:00+00:00', '2019-01-15 00:00:00+00:00',

...

'2019-08-14 00:00:00+00:00', '2019-08-15 00:00:00+00:00', '2019-08-16 00:00:00+00:00', '2019-08-19 00:00:00+00:00', '2019-08-20 00:00:00+00:00', '2019-08-21 00:00:00+00:00', '2019-08-22 00:00:00+00:00', '2019-08-23 00:00:00+00:00', '2019-08-26 00:00:00+00:00', '2019-08-27 00:00:00+00:00'], dtype='datetime64[ns, UTC]', name='split_0', length=160, freq=None), DatetimeIndex(['2019-04-24 00:00:00+00:00', '2019-04-25 00:00:00+00:00', '2019-04-26 00:00:00+00:00', '2019-04-29 00:00:00+00:00', '2019-04-30 00:00:00+00:00', '2019-05-06 00:00:00+00:00', '2019-05-07 00:00:00+00:00', '2019-05-08 00:00:00+00:00', '2019-05-09 00:00:00+00:00', '2019-05-10 00:00:00+00:00',

...

'2019-12-04 00:00:00+00:00', '2019-12-05 00:00:00+00:00', '2019-12-06 00:00:00+00:00', '2019-12-09 00:00:00+00:00', '2019-12-10 00:00:00+00:00', '2019-12-11 00:00:00+00:00', '2019-12-12 00:00:00+00:00', '2019-12-13 00:00:00+00:00', '2019-12-16 00:00:00+00:00', '2019-12-17 00:00:00+00:00'], dtype='datetime64[ns, UTC]', name='split_1', length=160, freq=None), DatetimeIndex(['2019-08-12 00:00:00+00:00', '2019-08-13 00:00:00+00:00', '2019-08-14 00:00:00+00:00', '2019-08-15 00:00:00+00:00', '2019-08-16 00:00:00+00:00', '2019-08-19 00:00:00+00:00', '2019-08-20 00:00:00+00:00', '2019-08-21 00:00:00+00:00', '2019-08-22 00:00:00+00:00', '2019-08-23 00:00:00+00:00',

...

'2020-03-26 00:00:00+00:00', '2020-03-27 00:00:00+00:00', '2020-03-30 00:00:00+00:00', '2020-03-31 00:00:00+00:00', '2020-04-01 00:00:00+00:00', '2020-04-02 00:00:00+00:00', '2020-04-03 00:00:00+00:00', '2020-04-07 00:00:00+00:00', '2020-04-08 00:00:00+00:00', '2020-04-09 00:00:00+00:00'], dtype='datetime64[ns, UTC]', name='split_2', length=160, freq=None)]

b,根据滑窗参数切分行情数据和信号

1 | (in_price, in_indexes), (out_price, out_indexes) = roll_in_and_out_samples(price, **split_kwargs) |

in_price.shape: (160, 11)

out_price.shape: (80, 11)

2019-01-02 00:00:00+00:00

2019-04-24 00:00:00+00:00

DatetimeIndex(['2019-03-25 00:00:00+00:00', '2019-03-26 00:00:00+00:00'], dtype='datetime64[ns, UTC]', name='split_0', freq=None)

###################

in_dmac_size.shape: (160, 8580)

in_dmac_size.iloc[:5,:5]:

split_idx 0

fast_window 10

slow_window 11 12 13 14 15

0 True True True True True

1 True True True True True

2 True True True True True

3 True True True True True

4 True True True True True

23,滑窗的收益数据计算

a,持有参数收益

在此区间,基础标的物表现

1 |

|

split_idx

0 0.235446

1 -1.630616

2 0.598889

3 2.647397

4 4.501923

Name: sharpe_ratio, dtype: float64

split_idx

0 -0.929956

1 2.065991

2 4.100300

3 4.801291

4 0.688785

Name: sharpe_ratio, dtype: float64

b,网格参数收益(训练集和验证集)

(8580,)

fast_window slow_window split_idx

10 11 0 0.235446

12 0 0.235446

13 0 0.235446

14 0 0.235446

15 0 0.235446

...

46 48 10 1.161184

49 10 1.325572

47 48 10 1.088731

49 10 1.129224

48 49 10 0.958552

Name: sharpe_ratio, Length: 8580, dtype: float64

(8580,)

fast_window slow_window split_idx

10 11 0 -0.703309

12 0 -0.703309

13 0 -0.703309

14 0 -0.929956

15 0 -0.929956

...

46 48 10 -0.119443

49 10 0.516152

47 48 10 -0.119443

49 10 -0.160922

48 49 10 -0.160922

Name: sharpe_ratio, Length: 8580, dtype: float64

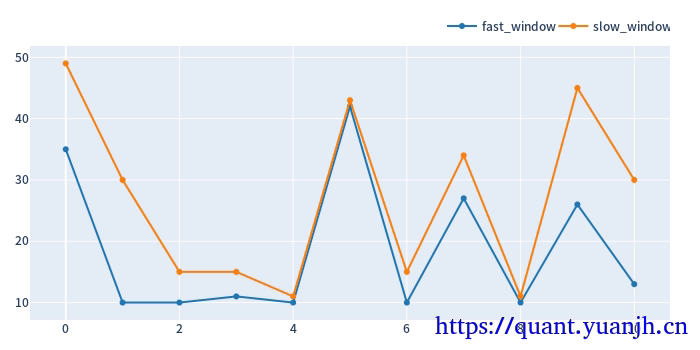

c,训练集上的最佳参数用于验证集

大致思路:

01,获取各split_idx的最佳收益(sharp_radio)的参数组合idxmax,也就是fast_window,slow_window,split_idx,三维索引元组

02,按照split_idx进行聚类,取得各split_idx对应的最佳参数。实际含义就是各滑动窗口的最佳参数

1 | def get_best_index(performance, higher_better=True): |

MultiIndex([(35, 49, 0),

(10, 30, 1),

(10, 15, 2),

(11, 15, 3),

(10, 11, 4)],

names=['fast_window', 'slow_window', 'split_idx'])

[[35 49]

[10 30]

[10 15]

[11 15]

[10 11]]

将滚动获取的最佳参数用于验证集,统计收益信息

1 | print('out_dmac_size.shape:',out_dmac_size.shape) |

out_dmac_size.shape: (80, 8580)

in_best_index.shape: (11,)

in_best_index: MultiIndex([(35, 49, 0),

(10, 30, 1),

(10, 15, 2),

(11, 15, 3),

(10, 11, 4),

(42, 43, 5),

(10, 15, 6),

(27, 34, 7),

(10, 11, 8),

(26, 45, 9),

(13, 30, 10)],

names=['fast_window', 'slow_window', 'split_idx'])

out_dmac_size.columns: MultiIndex([( 0, 10, 11),

( 0, 10, 12),

( 0, 10, 13),

( 0, 10, 14),

( 0, 10, 15),

( 0, 10, 16),

( 0, 10, 17),

( 0, 10, 18),

( 0, 10, 19),

( 0, 10, 20),

...

(10, 45, 46),

(10, 45, 47),

(10, 45, 48),

(10, 45, 49),

(10, 46, 47),

(10, 46, 48),

(10, 46, 49),

(10, 47, 48),

(10, 47, 49),

(10, 48, 49)],

names=['split_idx', 'fast_window', 'slow_window'], length=8580)

out_dmac_size.columns.names: ['split_idx', 'fast_window', 'slow_window']

in_best_index.names: ['fast_window', 'slow_window', 'split_idx']

out_dmac_size_reindexed[in_best_index].shape: (80, 11)

id col size entry_idx entry_price entry_fees exit_idx exit_price exit_fees pnl return direction status parent_id

0 0 0 199.762836 0 49.934525 24.937656 79 46.85 0.0 -641.111119 -0.064271 0 0 0

1 1 1 222.599259 0 44.811750 24.937656 79 58.80 0.0 3088.836429 0.309656 0 0 1

2 2 2 182.338041 0 54.706425 24.937656 79 88.73 0.0 6178.854345 0.619430 0 0 2

3 3 3 114.462060 0 87.147325 24.937656 79 183.53 0.0 11007.221874 1.103474 0 0 3

4 4 4 59.581957 0 167.417500 24.937656 79 176.88 0.0 538.856616 0.054020 0 0 4

5 5 5 56.155465 0 177.632975 24.937656 79 250.50 0.0 4066.944030 0.407711 0 0 5

6 6 6 39.282222 0 253.933250 24.937656 79 321.74 0.0 2638.662163 0.264526 0 0 6

7 7 7 33.080178 35 301.541975 24.937656 79 240.60 0.0 -2040.909064 -0.204601 0 0 7

8 8 8 41.989226 0 237.562425 24.937656 79 314.89 0.0 3221.987364 0.323004 0 0 8

9 9 9 33.376449 0 298.865300 24.937656 79 274.21 0.0 -847.844011 -0.084996 0 0 9

10 10 10 39.143143 44 254.835500 24.937656 79 266.59 0.0 435.170415 0.043626 0 0 10

fast_window slow_window split_idx

35 49 0 -0.929956

10 30 1 2.065991

15 2 4.100300

11 15 3 4.801291

10 11 4 0.688785

Name: sharpe_ratio, dtype: float64

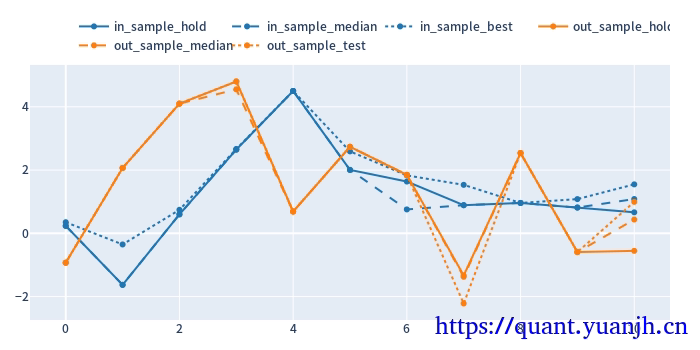

24,sharp ratio的汇总可视化

1 | cv_results_df = pd.DataFrame({ |

关注点:

蓝色部分

正常排序是(从上到下):点线,实现,线段,

橘色部分

实线对实线

说明测试集和验证集的周期收益情况,二者同时出现0轴同侧较好(同时上涨,同时下跌,保持行情的稳定性or延续性)

线段对线段

二者一方面随着各自颜色的实线趋势变化(受各自实线影响较大),其他应该无必然联系

点线对点线

蓝色点高于橘色点线,蓝色是训练集内最佳,橘色则是训练集得到最优参数用于验证集结果收益,大概率低于验证集。

测试,验证集时间长度差异,引入偏差

由于测试集一般是验证集的2-3倍(或更多),对于单边行情(假如上涨),则(测试集的)实线收益。蓝色线大概率位于橘色线上方。

如果下跌,则相反。蓝色由于时间长,大概率位于橘色下方。

注意:

01,202406,对于当前case,y周取值为sharp ratio夏普比,而非收益率。所以数据点高低并不反映收益率。

所以,以上结论需要稍斟酌,并不完全准确。

25,滚动回测收益可视化

1 | # 验证集:原始价格变动 |

out_price_org shape: (11,)

split_idx

0 0.940574

1 1.315436

2 1.625985

3 2.111239

4 1.059162

dtype: float64

############

out_hold_return shape: (11,)

split_idx

0 -0.064111

1 0.308884

2 0.617885

3 1.100722

4 0.053886

Name: total_return, dtype: float64

############

out_test_return shape: (11,)

fast_window slow_window split_idx

35 49 0 -0.064111

10 30 1 0.308884

15 2 0.617885

11 15 3 1.100722

10 11 4 0.053886

Name: total_return, dtype: float64

可见,整体结果尚可,上涨幅度基本吃到位,由于单纯依赖技术指标退出,没有止损。所以回撤也是无法避免的。

进一步思考

(非滚动模式)网格参数寻优得到的固定参数,其实是使用未来信息的(未来行情),不符合实际,也就是实际上无法落地。(5月份时,无法知道未来5-10月份,某个参数会取得较好收益)

滚动的网格参数寻优更符合实际,不含未来信息(可落地)。

时间周期越长,基于(非滚动模式)网格参数寻优取得较高收益概率越大,本质上是对历史的拟合。

但是滚动的测试未必,由于其未使用未来信息,如果策略本身无效,则大概率围绕0波动,类似随机。

26,计算正确性验证(略)

a,准备校验数据,数据展示

b,行情->指标 计算正确

0

23

26

22

24

28

c,指标->信号 计算正确

d,信号->交易 计算正确