基于vectorbt的基础唐奇安通道

09dc_01basic:基础方法

09dc_01basicV2:和基础方法等价,不过是基于vectorbt的指标机制的集成的dch指标。

01,基础配置信息

1 | #conda envs:vectorbt_env |

02,行情获取和可视化

a,时间交易参数配置

1 | # Enter your parameters here |

b,获取行情和行情mask

1 | # Download data with time buffer |

origin ohlcv_wbuf size: (1409, 5)

Index(['Open', 'High', 'Low', 'Close', 'Volume'], dtype='object')

wobuf_mask ohlcv size: (485, 5)

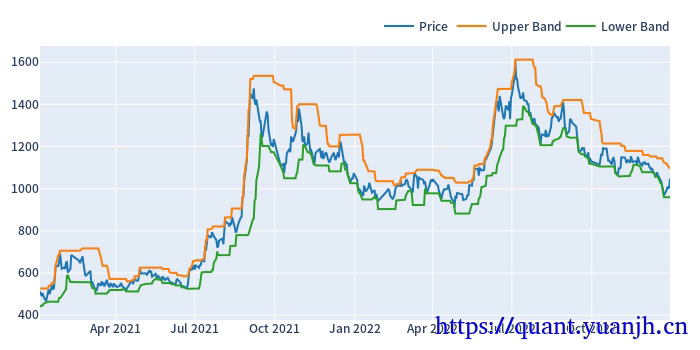

03,指标计算和可视化

1 | # fig.show_svg() |

(1409,)

(1409,)

(485,)

(485,)

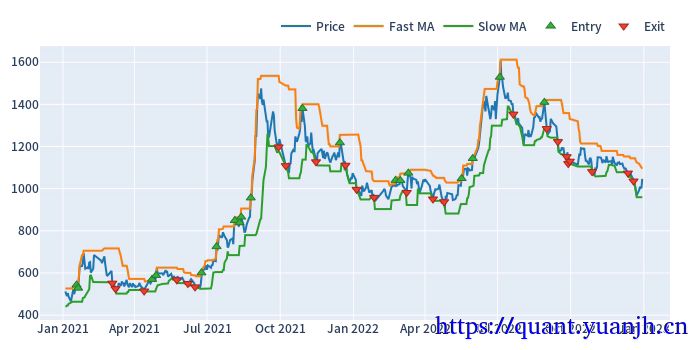

04,信号计算和可视化

1 | # def crossed_above(series1, series2): |

Start 2021-01-04 00:00:00+00:00

End 2022-12-30 00:00:00+00:00

Period 485

Total 19

Rate [%] 3.917526

Total Overlapping 0

Overlapping Rate [%] 0.0

First Index 2021-01-18 00:00:00+00:00

Last Index 2022-08-29 00:00:00+00:00

Norm Avg Index [-1, 1] -0.19552

Distance -> Other: Min 3.0

Distance -> Other: Max 67.0

Distance -> Other: Mean 25.315789

Distance -> Other: Std 17.34952

Total Partitions 19

Partition Rate [%] 100.0

Partition Length: Min 1.0

Partition Length: Max 1.0

Partition Length: Mean 1.0

Partition Length: Std 0.0

Partition Distance: Min 2.0

Partition Distance: Max 61.0

Partition Distance: Mean 21.722222

Partition Distance: Std 18.549792

dtype: object

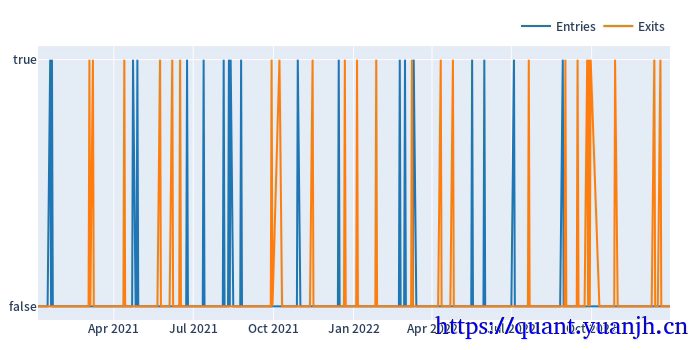

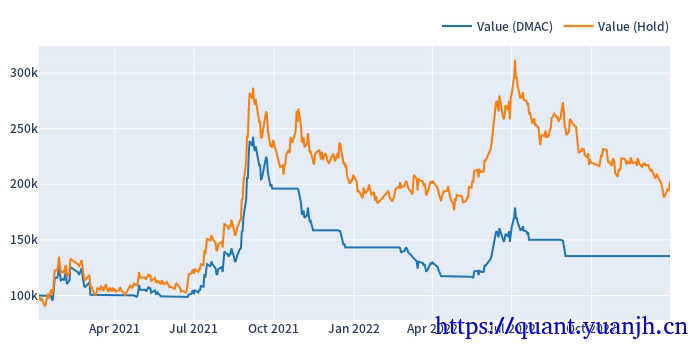

05,交易统计

a,基准比对

1 | dmac_pf = vbt.Portfolio.from_signals(ohlcv['Close'], dc_entries, dc_exits) |

Start 2021-01-04 00:00:00+00:00

End 2022-12-30 00:00:00+00:00

Period 485

Start Value 100000.0

End Value 135478.738311

Total Return [%] 35.478738

Benchmark Return [%] 104.325952

Max Gross Exposure [%] 100.0

Total Fees Paid 6084.898884

Max Drawdown [%] 52.33349

Max Drawdown Duration 318.0

Total Trades 9

Total Closed Trades 9

Total Open Trades 0

Open Trade PnL 0.0

Win Rate [%] 33.333333

Best Trade [%] 97.749209

Worst Trade [%] -19.171936

Avg Winning Trade [%] 42.098525

Avg Losing Trade [%] -9.811332

Avg Winning Trade Duration 47.0

Avg Losing Trade Duration 11.0

Profit Factor 1.374907

Expectancy 3942.082035

dtype: object

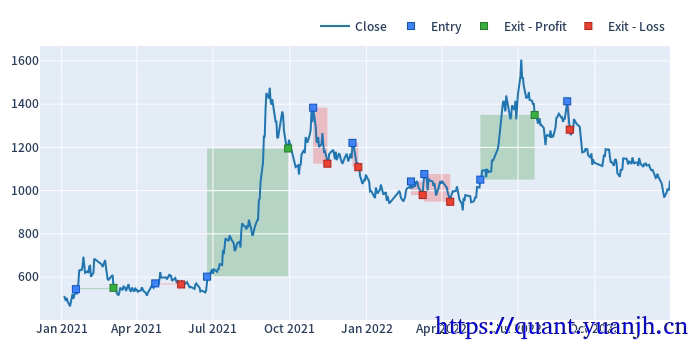

b,交易详情和可视化

1 | # Plot trades |

id col size entry_idx entry_price entry_fees exit_idx exit_price exit_fees pnl return direction status parent_id

0 0 0 183.350720 10 544.042715 249.376559 38 550.239953 252.217228 634.674170 0.006363 0 1 0

1 1 0 175.831773 73 570.907710 250.959287 91 565.963545 248.785934 -1369.086519 -0.013639 0 1 1

2 2 0 164.485565 113 601.986212 247.545106 180 1194.915225 491.365766 96789.353009 0.977492 0 1 2

3 3 0 141.336528 197 1383.690600 488.915064 208 1124.681250 397.396358 -37493.793739 -0.191719 0 1 3

4 4 0 129.545854 230 1220.924700 395.414331 235 1108.431975 358.981916 -15327.362345 -0.096907 0 1 4